First Watch Energy | Executive Insight – May 2026

From Concentrated Disruption to Strategic Repositioning

Why route security, LNG deliverability, and supply exposure are becoming central to oil and gas market confidence.

The global oil and gas system is no longer only reacting to disruption. It is beginning to reorganize around it.

What appeared in April as concentrated disruption has now evolved into a broader phase of strategic repositioning. Producers, operators, infrastructure networks, and service companies are adjusting to a market where supply risk is no longer temporary or isolated. It is becoming part of the operating environment.

In this setting, capacity alone is no longer enough. The central question is not simply who has resources, reserves, or production potential. The question is who can convert capacity into deliverable supply under pressure.

That distinction matters.

Oil and gas markets remain supported by resilient production in key basins, but reliability is increasingly shaped by route security, LNG deliverability, infrastructure resilience, export flexibility, and operator execution. The market is no longer rewarding scale alone. It is rewarding systems that can continue to move supply when pressure rises.

May shows a system entering a more active adjustment cycle.

Producers are recalibrating export strategies. Operators are prioritizing resilient offshore and LNG-linked developments. Infrastructure networks are becoming strategic assets rather than passive logistics channels. Service companies are aligning with complex projects where execution capability matters more than broad-based activity growth.

The result is a market increasingly defined by strategic confidence: the ability to sustain delivery, not merely announce capacity.

Why May Matters

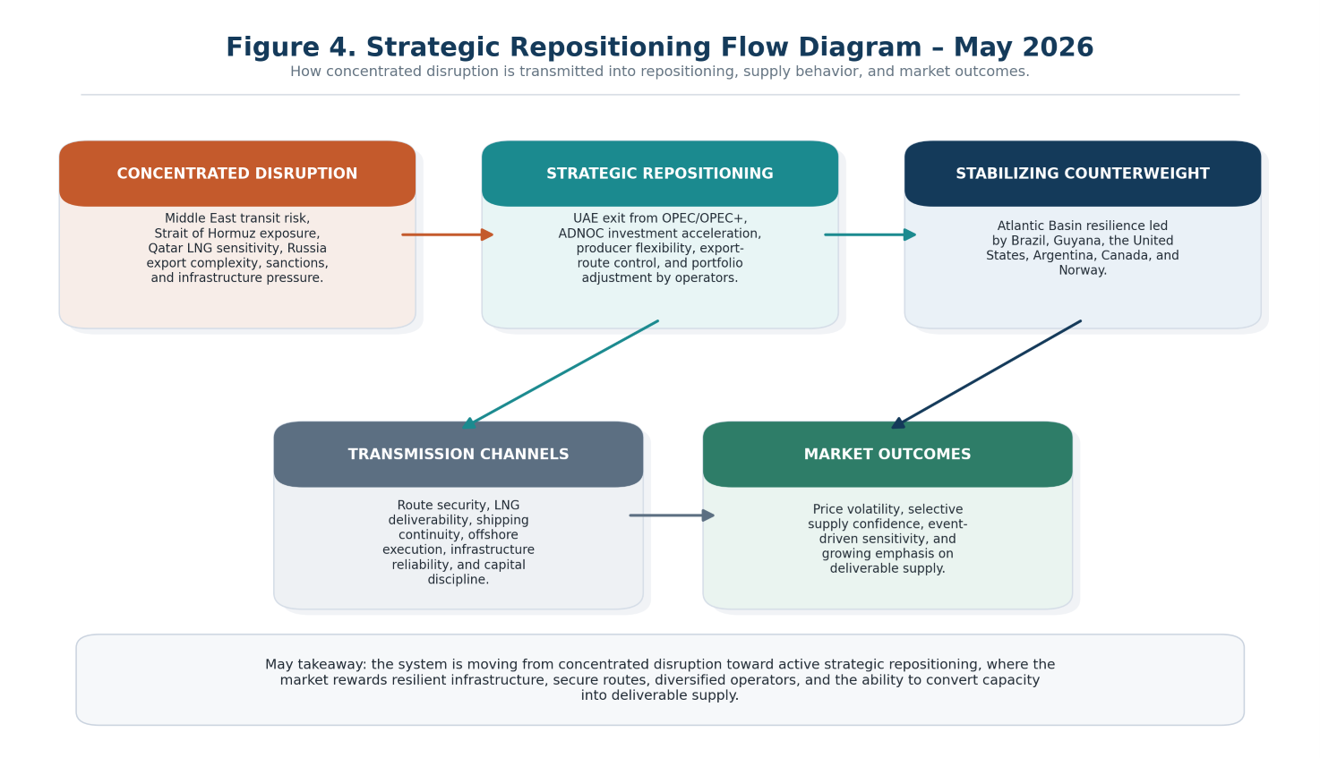

The defining signal in May is that disruption is no longer only a risk factor. It is now influencing how producers position themselves.

Several developments point in this direction.

The UAE’s exit from OPEC/OPEC+ and ADNOC’s accelerated investment strategy represent a shift toward more independent producer positioning. This does not eliminate the relevance of coordinated supply management, but it does show that some producers are increasingly focused on flexibility, capacity expansion, and strategic autonomy.

At the same time, Qatar’s LNG exposure reinforces the vulnerability of gas markets to regional disruption and export-route risk. LNG remains one of the most important pillars of global energy security, but its reliability depends heavily on infrastructure continuity, shipping routes, and the ability of suppliers to deliver under stress.

Russia continues to shape market complexity through sanctions exposure, export rerouting, opaque flows, and logistical adaptation. Its supply remains relevant, but the mechanisms through which barrels reach the market introduce uncertainty into pricing, routing, and long-term reliability.

Meanwhile, the Atlantic Basin continues to provide a stabilizing counterweight. Brazil, Guyana, Argentina, the United States, Canada, and Norway remain central to the reliability story because they combine production scale, project execution, infrastructure strength, and operator-led development.

This is the core of May’s message: disruption has not stopped supply growth, but it has changed how supply is valued.

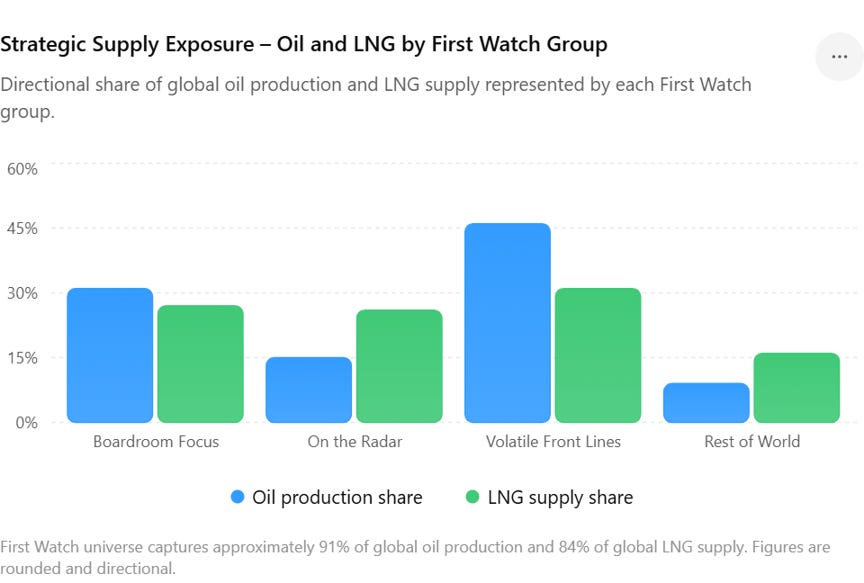

The Supply Exposure Signal

One of the most important additions to this month’s First Watch analysis is the Strategic Supply Exposure Metric.

The First Watch country universe captures approximately 91% of global oil production and 84% of global LNG supply. This does not mean that every country in the universe contributes equally, or that every producer carries the same reliability profile. It means that the countries tracked in First Watch represent a highly material share of the global oil and LNG system.

That matters because the analysis is not following a random list of countries. It is tracking a concentrated supply universe where changes in execution, infrastructure, policy, export capacity, sanctions exposure, or geopolitical risk can influence global market confidence.

The metric also helps clarify the difference between exposure and reliability.

Some countries contribute heavily to global supply and also provide strong planning confidence. Others contribute materially but remain vulnerable to sanctions, instability, route constraints, infrastructure exposure, or strategic producer shifts.

This is why First Watch separates the system into different analytical layers.

Reliable supply anchors provide the highest level of confidence. Execution-driven growth markets offer opportunity, but their contribution depends on milestones, capital continuity, infrastructure readiness, and policy alignment. Disruption-exposed producers remain influential because of scale, but their market impact is increasingly shaped by volatility.

In other words, the question is not only how much supply a country has.

The question is how dependable that supply is under pressure.

Reliability Is Becoming an Execution Advantage

In the current market, reliability is no longer a passive attribute. It is becoming an execution advantage.

A producer is not reliable simply because it has reserves. A basin is not reliable simply because it has resources. A project is not reliable simply because it has been sanctioned.

Reliability now depends on a broader set of conditions:

secure routes, resilient infrastructure, credible operators, regulatory continuity, LNG deliverability, export optionality, and the ability to sustain operations during disruption.

This is why countries such as Brazil and Guyana continue to matter. Their offshore growth is not only about production additions. It is about execution confidence. Projects are moving forward, operators are delivering, and supply is being converted into barrels with increasing consistency.

Argentina also remains important because Vaca Muerta continues to strengthen its role as a growth engine. Its contribution is still linked to infrastructure, export capacity, and capital discipline, but the direction is strategically relevant.

The United States and Canada continue to provide scale, infrastructure depth, and market flexibility. Norway remains a benchmark for institutional reliability and offshore continuity.

Together, these producers form a supply layer that markets can plan around.

By contrast, several large producers remain influential but harder to rely on as baseline supply assumptions. Sanctions, regional instability, export constraints, LNG exposure, and infrastructure vulnerability can rapidly alter market behavior. In these cases, scale remains important, but deliverability is conditional.

That is the distinction May makes clearer.

Capacity can exist on paper. Confidence only exists when capacity can move.

What Strategic Repositioning Looks Like

Strategic repositioning is not a single event. It is a pattern.

It appears when producers seek greater export flexibility. It appears when operators concentrate capital in more resilient basins. It appears when LNG becomes both a growth platform and a source of vulnerability. It appears when pipeline access, shipping routes, and offshore infrastructure become central to market confidence.

In May, this repositioning can be seen across several channels.

Producer strategy is shifting as countries respond to supply risk and market uncertainty. Some producers are seeking greater independence in production and investment decisions. Others are working to preserve coordination while managing exposure to disruption.

Operator execution remains concentrated among supermajors, national oil companies, and specialized players capable of delivering complex projects. Offshore growth in Brazil and Guyana, Vaca Muerta development in Argentina, LNG-linked activity across Asia and the Middle East, and frontier momentum in Namibia and Suriname all point to a market where growth remains active but selective.

The service sector is also adjusting. Demand is not being driven by broad activity recovery alone. It is increasingly linked to offshore execution, gas and LNG infrastructure, digital capability, completions efficiency, and complex project delivery.

Infrastructure has become one of the most important strategic variables. Routes, terminals, FPSOs, pipelines, LNG facilities, and export corridors now shape how markets interpret supply reliability.

This is the new operating logic: disruption is transmitted through infrastructure, route security, shipping continuity, offshore execution, and producer flexibility. The market response depends on whether supply can still move through that system.

Executive Takeaway

The May signal is clear.

The oil and gas system is not running out of capacity. It is becoming more selective about which capacity deserves confidence.

That is a very different market.

In a stable environment, scale can be enough. In a disruption-shaped environment, scale must be supported by infrastructure, execution, security, and deliverability.

The strongest positions will be built around producers, operators, and service providers that can convert opportunity into supply under pressure. The weakest positions will be those that depend on capacity that cannot reliably reach the market.

This is why strategic repositioning matters.

It reflects a market where producers are adapting, operators are prioritizing execution resilience, LNG is becoming more central to energy security, and infrastructure is becoming a competitive advantage.

For decision-makers, the implication is straightforward:

Do not evaluate oil and gas markets by capacity alone.

Evaluate them by deliverable supply.

First Watch Energy – Independent Oil & Gas Intelligence

Executive Insight based on the May 2026 First Watch Monthly Pulse.