First Watch: Key International Oil & Gas Developments | April 2026

Global upstream activity, market dynamics, and strategic developments shaping supply and resilience.

Editor’s Note

The global energy system has moved from distributed risk into a phase of concentrated disruption.

What emerged in March as operational stress has now evolved into a more structured environment where supply reliability is shaped by geographic exposure, infrastructure vulnerability, and execution resilience.

Oil markets remain supported—but increasingly sensitive to disruptions in a limited number of system-critical regions, particularly across key Middle East corridors.

Stability remains present—but it is no longer evenly distributed.

For decision-makers, the signal is clear:

Reliability is now defined by the ability to operate within disruption, not outside of it.

Executive Summary – A System Under Concentrated Disruption

April marks a decisive shift in the global oil and gas system. Disruption is no longer broadly distributed—it is now concentrated within a limited number of high-impact regions.

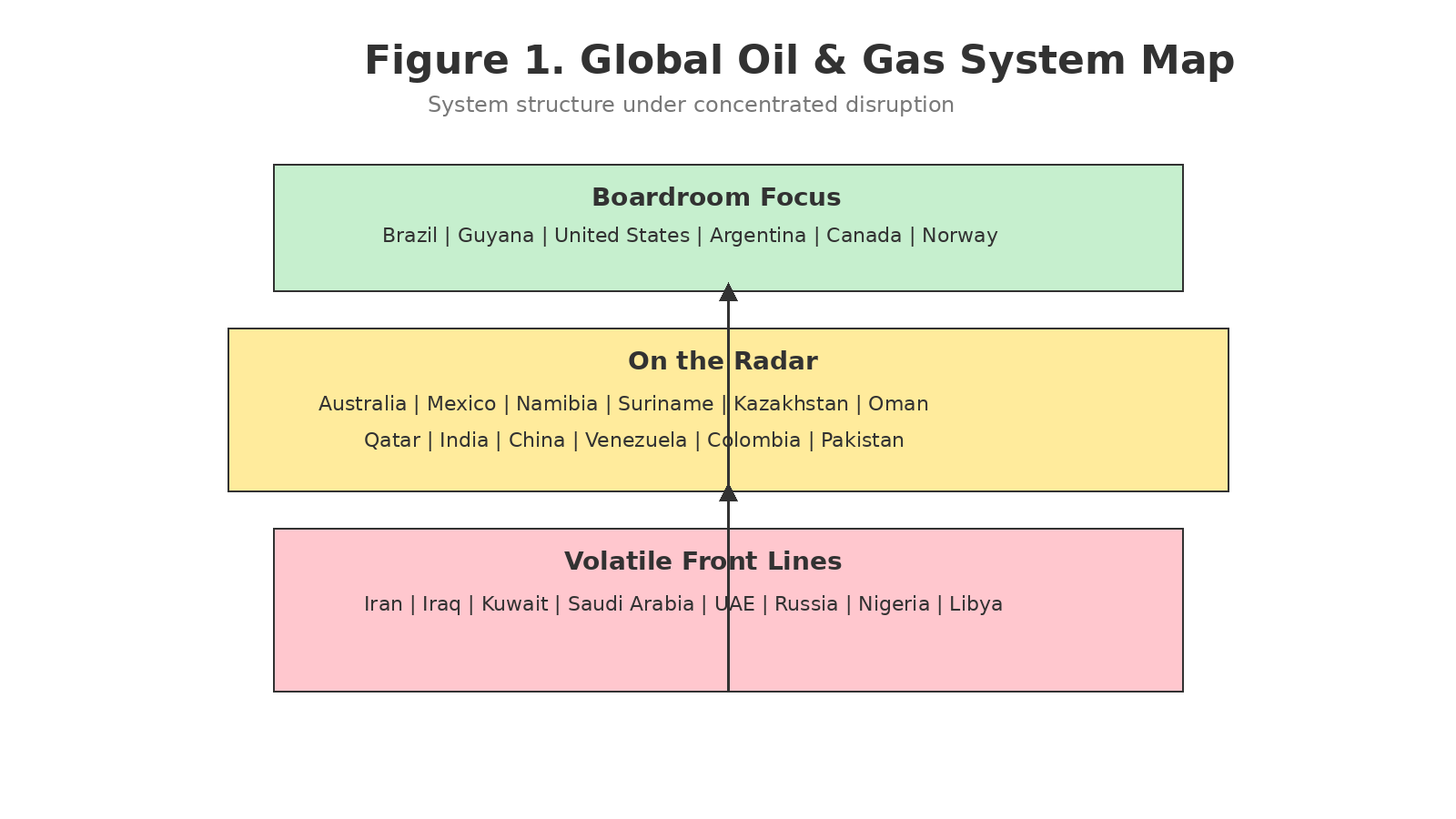

The system is structured across three distinct tiers:

Resilient Supply Anchors – Execution-proven producers sustaining delivery under pressure

Execution-Driven Opportunity – Markets with upside dependent on infrastructure and policy alignment

Concentrated Disruption – Producers directly influencing supply volatility through instability

Reliability is no longer defined by available capacity alone. It is increasingly determined by:

Geographic exposure

Infrastructure resilience

Execution capability under stress

Executive Outlook – Resilience Under Disruption

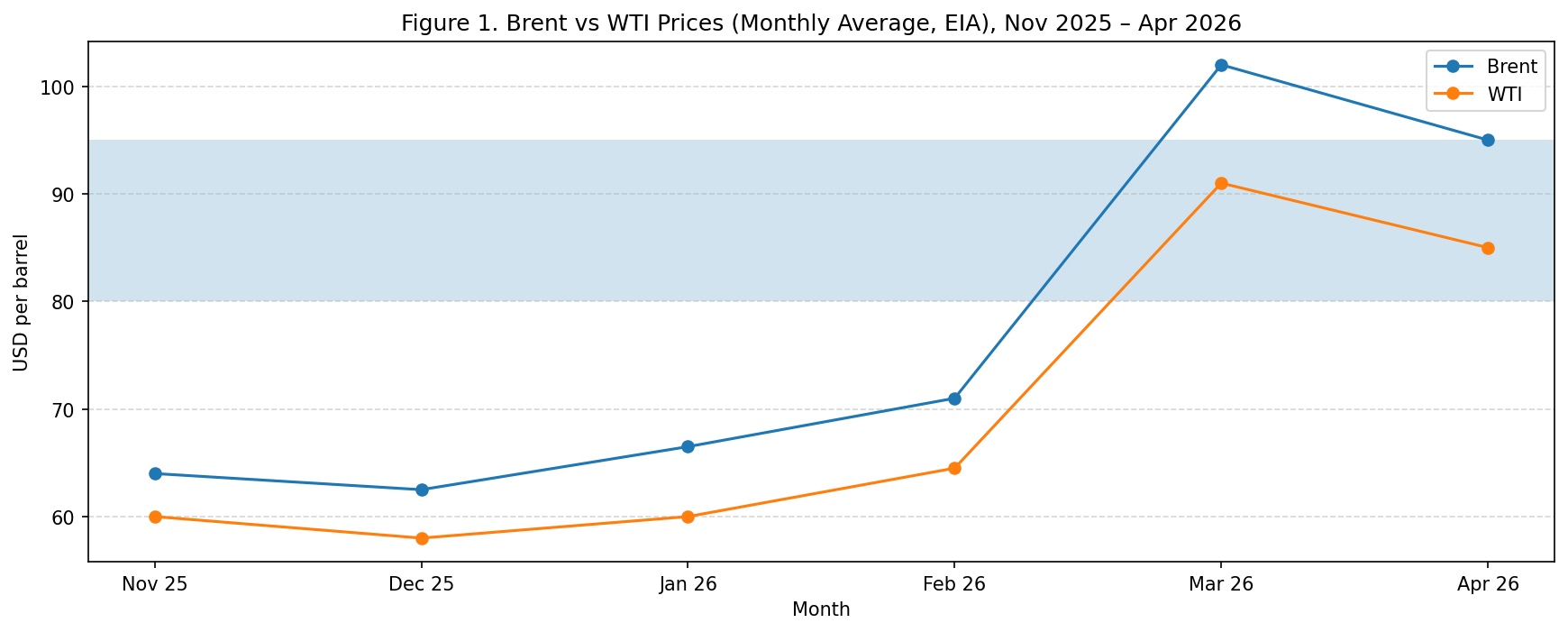

Looking ahead, the system is expected to remain supported within an elevated, volatility-sensitive price environment.

Supply growth continues—but remains selective

Geopolitical exposure is increasingly concentrated

System tolerance for disruption is declining

Oil markets are expected to operate broadly within the $80–$95 range, with disruption-driven spikes toward or above $100 per barrel.

The defining characteristic of this cycle is clear:

Stability is uneven and continuously tested.

Boardroom Focus – Proven Resilience Under Disruption

A refined group of producers now defines the system’s core supply anchors, demonstrating the ability to sustain delivery under active disruption:

Brazil – Offshore execution and pre-salt growth

Guyana – Consistent, operator-led production expansion

United States – Stable, uninterrupted output

Argentina – Vaca Muerta-driven growth and export momentum

Canada – Infrastructure strength and long-cycle stability

Norway – Institutional reliability and uninterrupted offshore production

What distinguishes this group is not scale—but execution continuity under pressure.

Credibility is no longer based on capacity—it is earned through delivery.

On the Radar – Execution-Driven Growth Under Constraint

A second tier of producers continues to offer strategic upside, though increasingly conditioned by execution:

Australia, Mexico, Kazakhstan, Oman

Namibia, Suriname, Colombia, Pakistan

China and India (demand-driven influence)

These markets are not limited by resource potential—but by their ability to convert opportunity into reliable, deliverable supply.

Opportunity exists—but must be validated through execution.

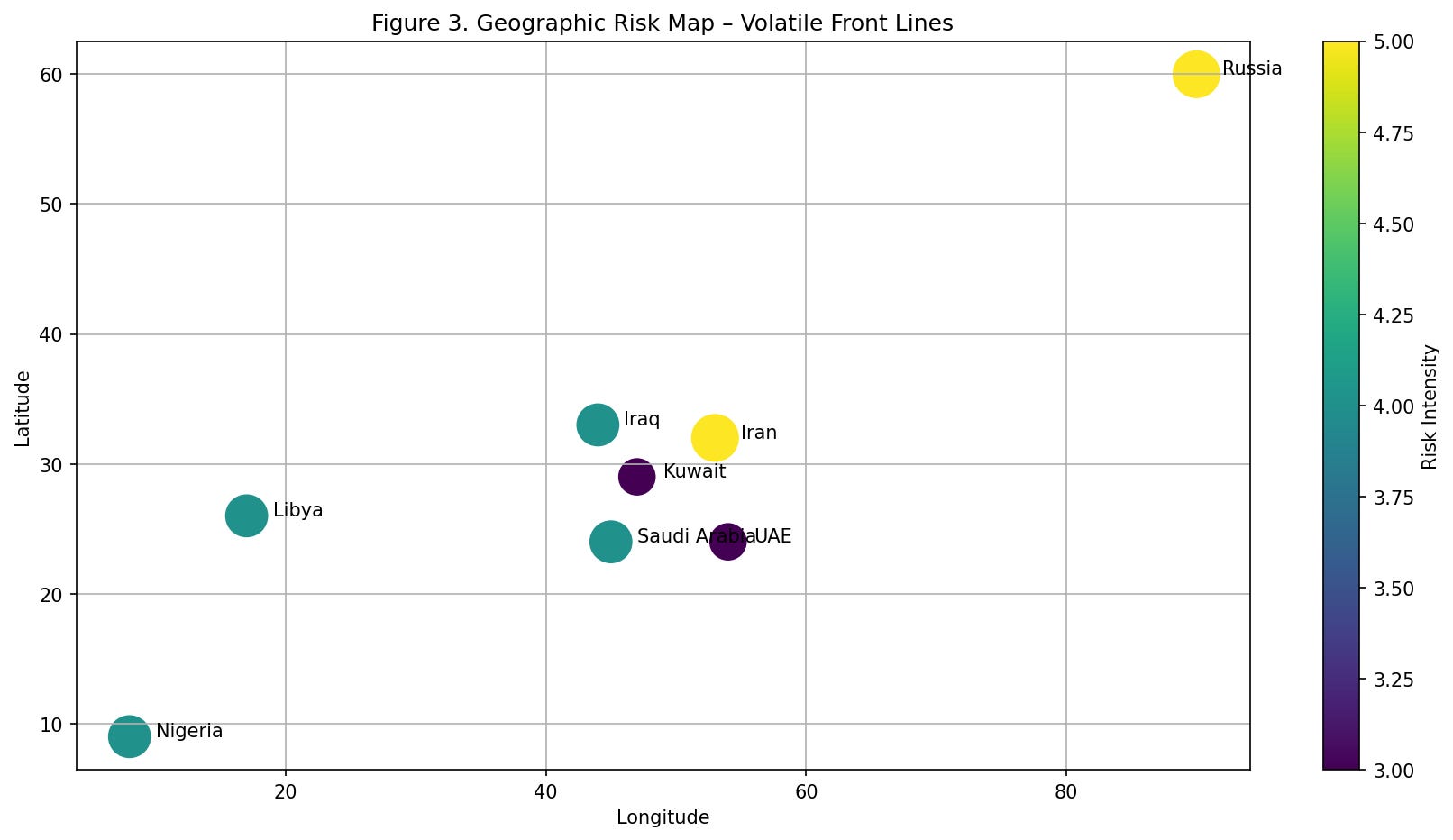

Volatile Front Lines – Disruption as a System Driver

The most significant shift in April is the concentration of disruption within system-critical regions.

Key pressure zones:

Middle East – High exposure across production and transit corridors

Russia – Infrastructure disruption and export complexity

Africa (Nigeria, Libya) – Recovery constrained by structural instability

Even traditionally stable producers are experiencing increased exposure to:

Security incidents

Infrastructure vulnerabilities

Export disruptions

Volatility is no longer episodic—it is embedded and system-defining.

Operator Landscape – Execution Concentration

Global supply continues to be driven by a concentrated group of operators:

Supermajors

ExxonMobil, Shell, TotalEnergies, Chevron, Equinor

National Champions

Petrobras, Saudi Aramco, ADNOC, QatarEnergy

Execution is increasingly defined by:

Offshore and LNG-linked developments

Capital discipline and long-cycle investment

Geographic diversification

Supply is no longer defined by geography—it is defined by execution capability.

Industry Pulse – International Execution Under Disruption

The oilfield services sector remains aligned with international and offshore growth.

Key players:

SLB – Integrated and technology-driven execution

Halliburton – Expanding international footprint

Baker Hughes – LNG and gas infrastructure leadership

Weatherford – Production optimization and recovery

Key dynamics:

International markets drive activity

North America remains disciplined

Projects are increasingly complex and capital-intensive

Growth persists—but is defined by execution, efficiency, and adaptability.

Global Signals – Concentration of Risk and System Impact

The system is now shaped by a tight set of interconnected risk factors:

Middle East corridors → High-impact disruption sensitivity

Russia flows → Structural pressure on exports and refining

Atlantic Basin growth → Partial but gradual rebalancing

LNG expansion → Supports diversification, but remains exposed

Oil markets reflect this structure:

Supported in the mid-$80s to low-$90s per barrel

Increasingly driven by real-time geopolitical events

The system is no longer broadly fragile—it is selectively sensitive.

Closing Signals – From Capacity to Reliability

April confirms a fundamental shift in how the global energy system operates.

This is not a system constrained by resource availability—but by reliability under pressure.

Capacity remains present

Investment continues

But deliverability is no longer guaranteed

A smaller group of execution-proven producers now defines stability, while disruption remains concentrated and highly impactful.

For operators, service companies, and decision-makers:

Scale is no longer sufficient

Execution consistency is critical

Diversification is essential

In a disruption-shaped system, reliability—not capacity—defines strength.

Closing Notes

First Watch Energy – Independent Oil & Gas Intelligence

Santiago Estefania

santiago@firstwatch.energy

www.firstwatch.energy

About First Watch

First Watch Energy – Independent Oil & Gas Intelligence

Delivering strategic insight into global upstream activity, market dynamics, and execution trends shaping the energy system.